Sports Betting & Price Sensitivity

The recent surcharge announcement and then reversal by DraftKings has invigorated conversation about price sensitivity in sports betting.

Intro to Price Sensitivity

Price sensitivity, or price elasticity of demand, measures changes in consumer purchasing behavior as prices move up and down. Generally, price and demand are inversely related–as price goes up, demand goes down. If the cost of pizza increases, we buy fewer slices or opt for an alternative.

Typically, businesses can discuss price sensitivity in a straightforward manner ("If we raise the price of popcorn by 1%, we will sell 3% fewer units.”)

What is the cost of a bet?

When it comes to wagering at a sportsbook, casino, or lottery, the topic of price sensitivity is less clear-cut, in part because the true "cost" of a bet is more obscure than that of a traditional purchase. While the financial cost of a $1 box of popcorn is obviously $1, what is the financial cost of a $1 blackjack hand, lottery ticket, or investment in the stock market?

A naive method for assessing cost could focus on the number of dollars risked to win a fixed amount. At first glance, risking $120 to win $100 feels more "expensive" than risking $80 to win $100. Additionally, the amount wagered is no longer available for other forms of consumption, thus a wager that is larger or longer in duration has a greater opportunity cost.

These features may contribute to two related, empirically-observed phenomena:

The “favorite-longshot bias” whereby bettors overvalue longshots and undervalue favorites

People overestimating the frequency of infrequent events and underestimating the frequency of frequent events

Expected Value

A more statistically accurate framing is to define the cost of the bet as the house edge or the bet's expected value.

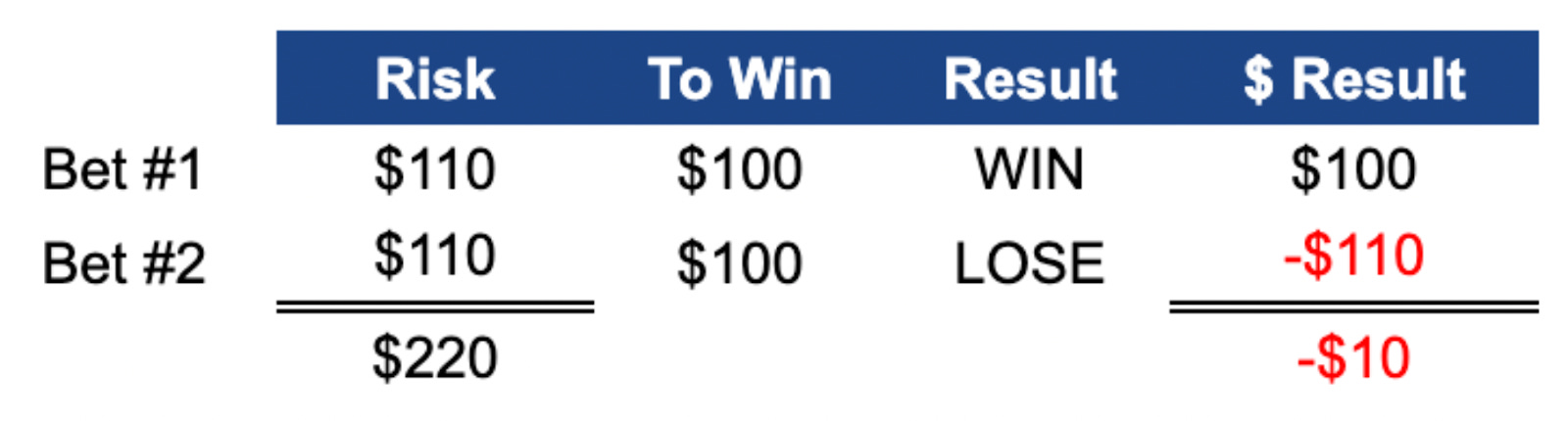

For example, suppose we place two wagers on 50/50 propositions at -110. We win one and lose one for a total of $220 risked and $210 returned, a net $10 loss.

From our perspective, we paid $10 to participate in this pair of wagers, or $5 each.

Additionally, we incurred a "cost" of having $220 locked away during the period when these bets were pending. That money could have been earning risk-free interest or used to produce utility in another manner.

While the outcome of any two bets can’t be known in advance, we can be virtually certain of losing almost exactly $5 per wager on average across a sufficiently large sample size.

What is the value of a bet?

What do we get in return for the $10 we expect to “pay” to place two $110 wagers at -110 odds?

Instant membership in the fraternity of people who placed the same bet, a similar bet, or the opposite bet

The feeling that we have skin in the game and are part of the action

A shortcut to caring about and focusing on something that doesn’t materially impact our lives outside of the realm of entertainment

The pleasure of rational calculation and inexpensive fantasy

The opportunity to say “I told you so,” which is a lot more fun when money is on the line

While there is a small cohort of bettors who exhibit line-shopping behaviors and price-sensitive preferences, most bettors don't bother and often bet suboptimal odds. This confirms at least some degree of non-financial motivation in purchasing decisions. Specific motivations include:

Convenience

Reliability

Brand affinity

Depth and breadth of markets

Loyalty programs

Entertainment-Seeking

Compared to value-seekers, entertainment-seeking customers tend to pursue bets with much shorter durations and longer odds (higher payouts). They typically aim for short-term returns of at least 100%, such that a few percentage points of expected value in the form of inferior odds, a surcharge, taxes, or otherwise is a trivial consideration.

Under the philosophy that psychological value is real value, it appears micro bets and same-game parlays are both more profitable for operators and more enjoyable for customers. Parlays, which tend to offer customers more entertainment value but less economic value, now compose 60% of revenue in some states.

Conclusions

When users are motivated by non-financial benefits, operators with powerful brands and unique offerings can arbitrage the value of the experiences they are able to create with the cost it takes to create them, allowing for higher long-term profit margins without risking cannibalization or churn risk.

While many analysts model consumers as rational agents with a fixed share of disposable income allocable to betting, the reality is that a majority of consumers freely rotate spending among adjacent entertainment and leisure categories. DraftKings competes for share of wallet with Netflix, Fortnite, and TopGolf just as much as it does with FanDuel.

A recreational customer deciding between spending $25 at TopGolf or DraftKings is not likely to worry about a nominal decrease in expected return compared to much more heavily-weighted considerations such as:

Which option offers the most convenience?

How will I feel during and after my experience?

How will this decision impact the way I am perceived by others?

Which decision will more reliably produce my desired outcome?

Will this experience create memorable moments?

We expect gaming and media companies to lean increasingly heavily into experiences rooted in competitive entertainment that offer superior unit economics while delivering maximum value to core users.